Crypto Invoicing in 2026: The Decision Framework for Freelancers Who Are Done Losing Money to Wire Fees

A Singapore-based design studio sends a $5,000 invoice to a Toronto client. The client wires payment through their commercial bank. By the time the funds settle in the studio's account, the wire fee has eaten $42.65, the FX spread has swallowed roughly $175 at the typical 3.5% consumer-grade rate, and the receiving bank has skimmed another $15. The studio booked $5,000. The studio received about $4,767. That's a 4.3% haircut on a single transaction, and according to the World Bank Remittance Prices Worldwide Q2 2026 report, those fee averages are not outliers — they're the global mean.

The same $5,000 sent as USDC on Polygon costs roughly $0.27 in network fees plus about 0.3% DEX slippage if conversion is needed. Total friction: about $15.27. That's the math that makes crypto invoicing structurally inevitable for cross-border knowledge work. But here's where most guides oversimplify: the tool you choose can quietly reintroduce every cost you thought you were escaping — through custody, KYC chokepoints, and hidden conversion spreads. This guide is the decision framework, not the sales pitch.

Table of Contents

- Why Traditional Invoicing Bleeds Crypto-Native Workers Dry

- Custodial vs. Non-Custodial: The Architecture Choice That Decides Everything

- The Seven Features That Separate Real Crypto Invoicing Tools From Marketing

- Building a Crypto Invoicing Workflow That Doesn't Require You to Be a Crypto Expert

- The Hidden Cost Map: Spreads, Slippage, and Other Silent Killers

- WavePay vs. Nowpayments vs. CoinGate vs. Cryptomus vs. BTCPayServer: The Honest Comparison

- Your 14-Day Crypto Invoicing Launch Plan

Why Traditional Invoicing Bleeds Crypto-Native Workers Dry

The status-quo cost stack is not one fee — it's a layered ambush. Walk it with me on a real $5,000 international invoice and you'll see why crypto invoicing isn't an ideological preference for Web3 workers, it's an economic one.

The fee stack. Start with the wire itself: $42.65 is the global average for an outbound consumer wire, per the World Bank Remittance Prices Worldwide Q2 2026 report. Add the FX spread — 3.5% is the consumer-grade average banks bake into the conversion rate without disclosure. Add the receiving bank fee, typically $10-25. If your client routes through PayPal instead, the math gets uglier: 4.4% transaction fee plus a fixed fee plus a 3-4% currency conversion spread. On a $5,000 invoice, PayPal's all-in friction routinely exceeds $400.

The settlement gap. The Federal Reserve Bank of Philadelphia Payment Chartbook 2025 puts traditional cross-border average settlement at 2.1 days. Two days doesn't sound catastrophic until you're a freelancer running on monthly retainers, invoices cluster at month-end, and rent clears on the first. Cash flow timing is the silent killer of independent practice — and a two-day float, multiplied across ten clients, is structurally hostile to anyone without a credit cushion.

The platform-risk problem. PayPal and Stripe carry account-freeze risk that the U.S. Government Accountability Office report on international transfers flags as a recurring source of cost-of-business disruption. TOS violations, "high-risk industry" flags, sudden 180-day reserves — for NFT artists, Web3 developers, and crypto-adjacent freelancers, this isn't theoretical. Entire categories of legitimate work get reclassified as risky overnight.

The geographic gatekeeping issue. Stripe doesn't fully serve 80+ countries. PayPal restricts transfers in dozens more. A developer in Lagos invoicing a client in Berlin has very few clean traditional options — and the ones available charge the most.

The chargeback asymmetry. Traditional rails allow buyer-initiated reversals up to 180 days post-payment. For digital deliverables — design files, code commits, written content — this is structurally unfair to the freelancer. Crypto's immutability flips the default: once confirmed, funds are yours, and disputes happen via communication rather than via the payment processor unilaterally reversing.

The regulatory passthrough. Sarah Johnson, Former Director of Financial Innovation at the Consumer Financial Protection Bureau, frames the deepest problem in her Brookings Institution analysis: "Custodial payment platforms create regulatory vulnerabilities for freelancers—when the platform is the money transmitter, your payment becomes subject to their regulatory compliance, not yours." Translation: when the platform's licenses lapse or its jurisdictional exposure shifts, your access to your money shifts with it. You inherit risk you didn't underwrite.

Stack these together on a freelancer running 50 invoices a year at an average $3,000 each. Traditional rails bleed somewhere between $4,000 and $7,000 annually in direct fees and forex spreads alone, before counting the settlement-gap cost of capital or the tail risk of a frozen account. Crypto solves the cost and speed problem. But which crypto invoicing model? That's where most freelancers stall — and lose money differently.

A $42 wire fee on a single invoice looks small. Multiply by fifty invoices a year and the freelancer who switched to stablecoin payments kept a vacation that the freelancer who didn't, did not.

Custodial vs. Non-Custodial: The Architecture Choice That Decides Everything

Every crypto invoicing decision downstream — fees, KYC, settlement speed, regulatory exposure, off-ramp friction — flows from one architectural choice. Get this right and the rest is configuration. Get it wrong and you've rebuilt PayPal with extra steps.

| Criteria | Custodial (Nowpayments, CoinGate, Cryptomus) | Non-Custodial (WavePay, BTCPayServer) |

|---|---|---|

| KYC required | Yes — typically above $900 withdrawal threshold | No |

| Wallet ownership | Platform holds funds | You hold funds |

| Settlement speed | 1–3 days to fiat; minutes to platform balance | Under 5 minutes to your wallet |

| Average fees | 2.5–3.5% + network | 0.5–1.0% network only |

| Counterparty risk | High — platform insolvency exposure | Zero |

| Cross-chain payer input | Limited to supported chains | Any chain (with aggregator routing) |

| Receiver token control | Limited — platform decides | Full — you choose |

| Conversion transparency | Opaque spreads baked in | On-chain, verifiable |

| Regulatory classification | Likely VASP under FATF guidance | Generally not VASP |

| Best fit | Fiat exit speed, non-technical users | Crypto-native workflows, multi-jurisdiction |

Fee and settlement benchmarks: Blockchain Association Payment Processor Benchmark Report 2026.

The regulatory column matters more than it looks. The FATF Updated Guidance on Virtual Assets and VASPs is steadily pulling custodial crypto payment processors into the same KYC/AML regime as banks. The trajectory is one-directional: every year, custodial platforms tighten verification thresholds, expand reporting obligations, and shorten the window before a "lite" account becomes a "full" account. The "easy crypto" promise that made custodial platforms attractive in 2019 is being legislated out of existence.

Counterparty risk isn't abstract either. The industry pattern is well-established — custodial platforms freeze withdrawals during liquidity events, get caught in jurisdictional disputes, or simply fail. When your funds sit on their balance sheet, you are an unsecured creditor with no deposit insurance. Johnson's Brookings framing matters here: the freelancer's regulatory exposure is no longer the freelancer's own — it's whatever the platform's exposure looks like on the worst day of the year.

The decision rule is uncomfortably clean. If you need fiat in your bank account this week, you're already KYC-comfortable, and your client base is regulatorily uncomplicated — custodial works. If you operate across borders, want to stay in crypto for any portion of your workflow, hold strong views on privacy, or work in any category a payment processor might unilaterally reclassify as risky — non-custodial is the only honest answer. There is no middle path that preserves the benefits of both. Architecture is destiny.

The Seven Features That Separate Real Crypto Invoicing Tools From Marketing

Once you've picked your architecture, the next filter is feature reality. Marketing copy is generous. Production behavior is not. These seven features determine whether your invoicing setup is solid or theatrical.

| Feature | Impact | What Breaks Without It | Who Has It |

|---|---|---|---|

| Cross-chain payer input | Critical | Client on Arbitrum can't pay your Polygon invoice; deal dies | WavePay (1inch Fusion+); few others |

| Receiver token control | Critical | You absorb whatever they sent; manual swap costs 0.3–2% | WavePay; not BTCPayServer (BTC-only) |

| On-chain conversion transparency | Critical | Hidden 1–3% spread per invoice | Non-custodial with DEX aggregator routing |

| KYC-free generation | High | Privacy compromised; jurisdictional exposure | WavePay, BTCPayServer |

| Direct wallet settlement | High | Funds sit on platform; counterparty risk returns | Non-custodial only |

| Reusable payment links | Medium | Repeat clients need new link each invoice | Most modern platforms |

| Mobile payer UX | Medium | 60%+ of payers abandon if mobile flow breaks | Varies; test before committing |

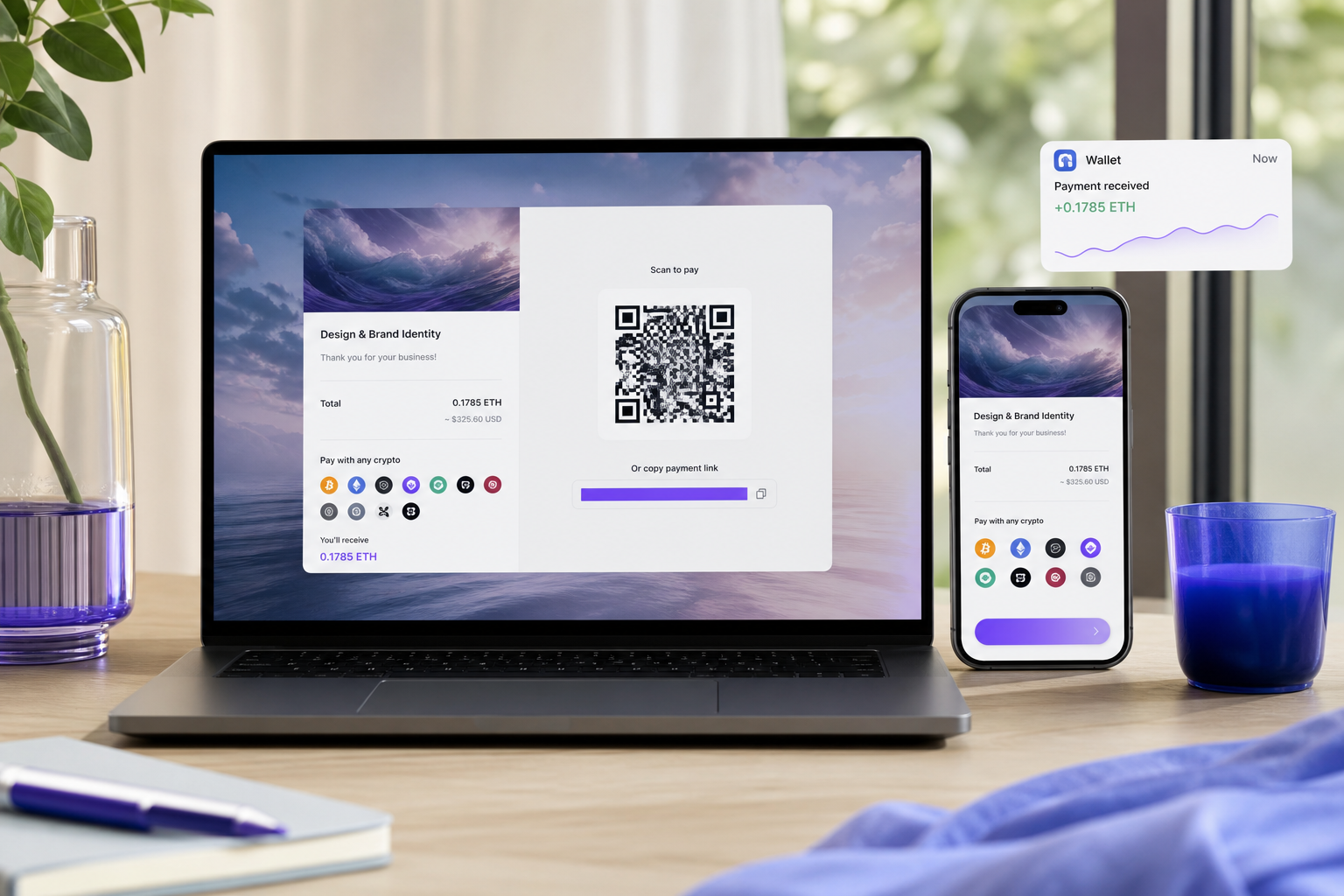

The standard underneath the table worth knowing: ERC-681 is the Ethereum specification for payment request URIs. In plain English: it's the standard that lets any Ethereum wallet recognize and parse a payment link without custom integration. When you generate a payment link compliant with ERC-681, MetaMask, Rainbow, Coinbase Wallet, and dozens of others all know what to do with it. When you generate a link in some proprietary format, half your clients hit "wallet not supported" and walk away.

Cross-chain payer input is the single highest-leverage feature on the list. The MIT Digital Currency Initiative Cryptocurrency Payment Usability Study 2025 found that 18% of crypto payments fail due to address or chain errors among new users — roughly one in five attempts. Cross-chain routing via aggregators like 1inch Fusion+ eliminates the failure mode entirely: the payer sends from where they are, you receive what you want, and the routing happens in a single transaction without manual bridging.

Walk a concrete scenario. Your client holds ETH on Arbitrum. You want USDC on Base. A traditional crypto checkout asks them to bridge first — bridge fee of 0.5%, ten-minute wait, possible failure that strands funds. An aggregator-routed link executes the whole path in one transaction with one signature. The client doesn't need to know what a bridge is. They click, they confirm, you receive USDC on Base.

Dr. Rebecca Chen, Associate Professor of Digital Finance at MIT Sloan School of Management, put the underlying principle plainly in her MIT Tech Review interview: "The greatest risk for freelancers accepting crypto isn't volatility—it's address errors and irreversible transactions." The single best risk-reduction lever you have is feature selection. Cross-chain support, receiver token control, and on-chain transparency are the non-negotiable triangle. Without all three, you're not invoicing in crypto — you're gambling in crypto.

The best crypto invoicing tool is the one you stop thinking about after setup — link generated, link shared, funds in wallet, work continues.

Building a Crypto Invoicing Workflow That Doesn't Require You to Be a Crypto Expert

You don't need a deep technical background to run professional crypto invoicing. You need a small number of decisions made once, documented, and stuck to. Six steps, in order.

Step 1: Pick your one receiving token and stick with it

Default to USDC. The Centre Consortium Attestation Framework requires monthly reserve audits by independent firms (Grant Thornton, BDO, and similar) maintaining 1:1 USD backing. USDT is acceptable in markets where USDC liquidity is thin, but transparency is materially lower. Stable purchasing power, universal acceptance, deep liquidity, minimal slippage — that's the USDC case.

Common mistake: accepting ETH or BTC on invoices "because it might go up." That's speculation, not invoicing. If you want directional exposure, buy it deliberately after settlement.

Step 2: Pick your one settlement chain

The decision rule:

- Polygon or Base if low fees are your priority (roughly $0.01–$0.10 per transaction)

- Solana if speed matters most — Abillio's platform documentation notes Solana operates at approximately 65,000 TPS with sub-cent fees, according to Abill.io [VENDOR SOURCE]

- Ethereum L1 only if a specific high-value client demands it

One chain means one set of confirmation expectations to learn, one block explorer to bookmark, one bridge mental model. Optionality is the enemy of operational simplicity.

Step 3: Provision a dedicated invoicing wallet

Create a fresh wallet — separate from your trading wallet, separate from your DeFi wallet. Why: IRS Notice 2025-43 requires capturing wallet addresses, transaction hashes, and USD value at time of transaction for every digital asset received. A clean, single-purpose wallet produces a clean, single-purpose ledger.

If your annual invoicing exceeds $10,000, move to a hardware wallet (Ledger or Trezor). The cost amortizes against a single avoided phishing incident.

Step 4: Generate and test the payment link

Send yourself $1 first. Always. Verify four things: the link loads correctly on mobile, the receiver token displays as expected, the conversion preview shows reasonable output for any input token, and the settlement lands at the expected confirmation count.

Confirmation counts you should memorize, from IEEE Standard 2418: roughly 32 confirmations for Solana finality, 12-15 for Ethereum, 128 for Polygon. The "should I treat this as paid yet" mental model lives in those numbers.

Step 5: Embed the link in your invoice template

Include both the payment link and a plain-text fallback: wallet address, token, chain name. Some payers' wallets don't yet handle ERC-681 cleanly. The fallback is your insurance.

Step 6: Configure notifications and archive

Webhook to Slack or Telegram. Failing that, email alerts on payment receipt. For every paid invoice, archive: client name, date sent, invoice number, expected amount, transaction hash. Two purposes — IRS audit defense and repeat-client operational efficiency. The second client invoice is half the work of the first only if you saved the artifacts of the first.

Once the workflow runs, the only risk left is invisible: the fees you don't see.

The Hidden Cost Map: Spreads, Slippage, and Other Silent Killers

Direct fees are easy to see and easy to optimize. The losses that compound are the ones you never noticed leaving. Five categories, each with a concrete dollar example and a mitigation.

The Conversion Spread Trap

Custodial platforms quote one rate and settle at another. The delta — typically 1-3% — is the platform's silent margin. On a $10,000 invoice, that's $100–$300 you never see leave your account because it never arrived. The Blockchain Association Payment Processor Benchmark Report 2026 puts the average custodial all-in cost at 2.5-3.5%, with the spread component being the majority of the gap above advertised fees. Solution: non-custodial routing via DEX aggregators shows you the swap math on-chain before you sign. If you can't see the rate, you're paying it.

The Stablecoin Depeg Window

USDC, USDT, and DAI target $1, but during liquidity crunches they can trade 0.97-1.02. The reference event remains March 2023, when USDC briefly traded to $0.87 during the Silicon Valley Bank exposure window. If you settle a large invoice through a market swap during a stress event, you eat the depeg. Solution: for invoices above roughly $25,000, use a limit order on a DEX like Uniswap rather than a market swap. Patience costs nothing. Slippage during stress costs whatever the market decides.

The Network Fee Wildcard

Polygon and Base average $0.01-$0.10 per transaction in normal conditions. Ethereum L1 has spiked above $50 during congestion events. If your invoice accidentally routes through a different chain than you intended — because your link wasn't explicit enough or the payer's wallet defaulted somewhere unexpected — fees compound fast. Solution: communicate your preferred chain explicitly on the invoice, both in the link and in the plain-text fallback.

The Tax Compliance Tax

The IRS 2025 cryptocurrency compliance data shows 68% of freelancers receiving crypto payments failed to properly report them. The downstream cost of getting this wrong — penalties, interest, audit hours, professional remediation fees — routinely exceeds the traditional payment fees the freelancer thought they were saving. Carlos Mendez, CPA and IRS-registered e-File provider, framed the gap in his Journal of Accountancy article: "Stablecoins on high-performance blockchains like Solana have solved the speed problem for cross-border payments, but the real challenge remains tax compliance education for independent workers." Solution: capture transaction hash plus USD-at-receipt for every invoice. Koinly, CoinTracker, or equivalent tools automate this — install one before your first invoice, not after your first audit letter.

The KYC-to-Fiat Bridge

You can stay KYC-free on the crypto side of your workflow. The moment you cash out to a bank account, the exchange will ask. Plan the off-ramp deliberately: Kraken and Coinbase are reliable but require full KYC; peer-to-peer venues like Bisq or LocalCryptos exist but carry counterparty risk and slower execution. Don't pretend the bridge doesn't exist — budget the time and the verification effort. Many freelancers solve this by holding 60-80% of their crypto receipts in stablecoin reserves and cashing out 20-40% quarterly through a single verified venue. One verified relationship, predictable cadence, minimal recurring friction.

A 1% hidden spread is invisible on one invoice. Across fifty invoices a year, it's the difference between profit and a side hustle that pays itself.

WavePay vs. Nowpayments vs. CoinGate vs. Cryptomus vs. BTCPayServer: The Honest Comparison

There is no universally "best" crypto invoicing platform. There is a best fit per workflow. The table shows where each platform genuinely wins — not where its marketing pretends it wins.

| Platform | Custody Model | KYC | Cross-Chain Input | Settlement |

|---|---|---|---|---|

| WavePay | Non-custodial | None | Yes (1inch Fusion+) | Under 5 min to wallet |

| Nowpayments | Custodial | Above $900 withdrawal | Limited | 1–3 days to fiat |

| CoinGate | Custodial | Yes | Some chains | 1–3 days to fiat |

| Cryptomus | Custodial | Yes | Limited | 1–3 days |

| BTCPayServer | Non-custodial, self-hosted | None | No — BTC-only | Instant |

| Platform | Receiver Token Choice | Fee Structure | Best Fit |

|---|---|---|---|

| WavePay | Yes — payer-agnostic | Network fee + transparent DEX slippage | Web3 creators, multi-chain freelancers |

| Nowpayments | Limited menu | 0.5% + opaque conversion spread | Fiat exit prioritized |

| CoinGate | Some tokens | ~1% + spread | European market, fiat invoicing |

| Cryptomus | Limited | Opaque spreads | Emerging markets payouts |

| BTCPayServer | No — BTC-only | Network fee only | Bitcoin maximalists with sysadmin skills |

Four scenarios clarify the choice.

The NFT artist on Foundation paid by collectors across Ethereum, Base, and Arbitrum. The platform's cross-chain routing via 1inch Fusion+ is structurally the only option that doesn't force the collector to bridge first. Custodial competitors either reject the payment outright or require manual bridging that loses 0.5%+ and frequently fails. BTCPayServer is a non-starter because Bitcoin-only doesn't match where NFT collectors actually hold liquidity.

The European e-commerce store wanting EUR settled to a bank account weekly. CoinGate is purpose-built for this. The custodial trade-off is genuinely acceptable here because fiat exit is the explicit goal, the EU regulatory framework is comparatively clear, and CoinGate's bank rails into European IBANs are mature. Don't fight the right tool for the wrong reasons.

The self-hosted Bitcoin-only merchant ideologically committed to no third parties. BTCPayServer is the unambiguous answer, accepting that the setup curve is steep — VPS provisioning, optional Lightning node operation, ongoing security maintenance. The reward is total sovereignty. The price is sysadmin time you may or may not want to spend.

The remote developer in a high-regulatory-risk jurisdiction. Non-custodial is mandatory, not preferred. The combination of no KYC, receiver token choice, and direct wallet settlement removes every regulatory chokepoint that custodial platforms reintroduce. Johnson's Brookings framing applies most sharply here: a custodial platform makes your payment legally dependent on their compliance posture. Non-custodial severs that dependency.

The honest counter-evidence: the MIT Digital Currency Initiative Implementation Study 2026 found 43% of small businesses report accounting software integration friction with crypto payments. Non-custodial platforms transfer integration burden to the user. Webhook configuration, transaction-hash capture, and reconciliation discipline don't happen automatically — they happen because you set them up. If you won't do that work, custodial may save you more in operational time than it costs in fees.

The structural takeaway: the question is not "which platform is best" — it's "what custody model fits my regulatory exposure, technical comfort, and off-ramp cadence?" For Web3-native workers, the answer collapses to non-custodial plus cross-chain plus transparent. Inside that bucket, the combination of 1inch Fusion+ routing and receiver token control has very few direct equivalents.

Your 14-Day Crypto Invoicing Launch Plan

Frame this as a launch, not a recap. Sixteen items, four phases, two weeks from cold start to live invoicing.

Days 1–2: Audit and Decide

1. Pull your last 12 months of invoices. Tally: number of clients, average invoice size, payment methods used, fees paid. This is your baseline — without it, you can't measure whether the switch worked.

2. Pick your receiving token. Default: USDC. Deviate only if you have a specific liquidity or jurisdictional reason.

3. Pick your settlement chain. Polygon or Base for fee priority. Solana for speed. Ethereum L1 only if a specific major client requires it.

4. Decide your off-ramp cadence. Three options: hold-in-stablecoin, partial-fiat-conversion (e.g., 30% quarterly), or full-cashout per invoice. Pick one. Write it down. Revisit only at the 90-day review.

Days 3–5: Provision and Test

5. Create or designate a dedicated invoicing wallet, separate from any trading or DeFi wallet. Single-purpose ledger, single-purpose tax recordkeeping.

6. If your annual invoicing exceeds $10,000, order a hardware wallet (Ledger or Trezor). Expect 3-5 business days to arrive. Order on day 3 so it's on your desk before day 8.

7. Generate your first payment link with the chosen token and chain.

8. Send yourself $1 through the link. Verify mobile load, conversion preview accuracy, settlement at expected confirmation count. If any step fails, fix it now — not under deadline pressure with a real client.

Days 6–10: Integrate

9. Add a crypto payment line item to your standard invoice template. Include the link, the receiving token name, the chain name, and a plain-text wallet address as fallback. Five lines maximum — clarity beats completeness.

10. Set up payment notifications. Webhook to Slack or Telegram is best. Email alerts as second choice. Silence on confirmation is operationally dangerous.

11. Install Koinly, CoinTracker, or equivalent. Connect your invoicing wallet read-only. Verify the tool captures transaction hash plus USD-at-receipt for every inflow — that's the IRS Notice 2025-43 requirement.

12. Write a one-paragraph "how to pay me in crypto" explainer for clients who've never done it. Keep it under 100 words. Save it as a snippet. You'll paste it dozens of times.

Days 11–14: Launch

13. Send your next real invoice with the crypto option included alongside your existing payment methods. Don't make crypto mandatory. Make it available.

14. Track friction on the first three payments. Did the client ask questions? Did the funds land in the expected window? What was the actual all-in cost versus the traditional rail you compared against?

15. After three successful crypto payments, retire the traditional-only version of your invoice template. The default should be crypto-available — friction lives at the default.

16. Schedule a 90-day review on your calendar now. Revisit token choice, chain choice, off-ramp cadence, and platform fit. Liquidity moves. Regulations move. Your workflow should too.

The freelancer who runs this plan in November invoices in crypto by December — and stops losing $200 per international wire by January.